Should You Buy a Car Outright, Finance It, or Use a Novated Lease?

- Mar 23

- 3 min read

Updated: May 11

One of the common questions we receive from clients is "how should I purchase my next vehicle?". The right answer depends on your tax situation, cashflow, interest rates, opportunity cost and individual circumstances! Funding a new vehicle can be done in many forms including by using savings, taking out a car loan or via a novated lease.

For clients who are also business owners, they have the additional options of funding the purchase using business cash or a business loan.

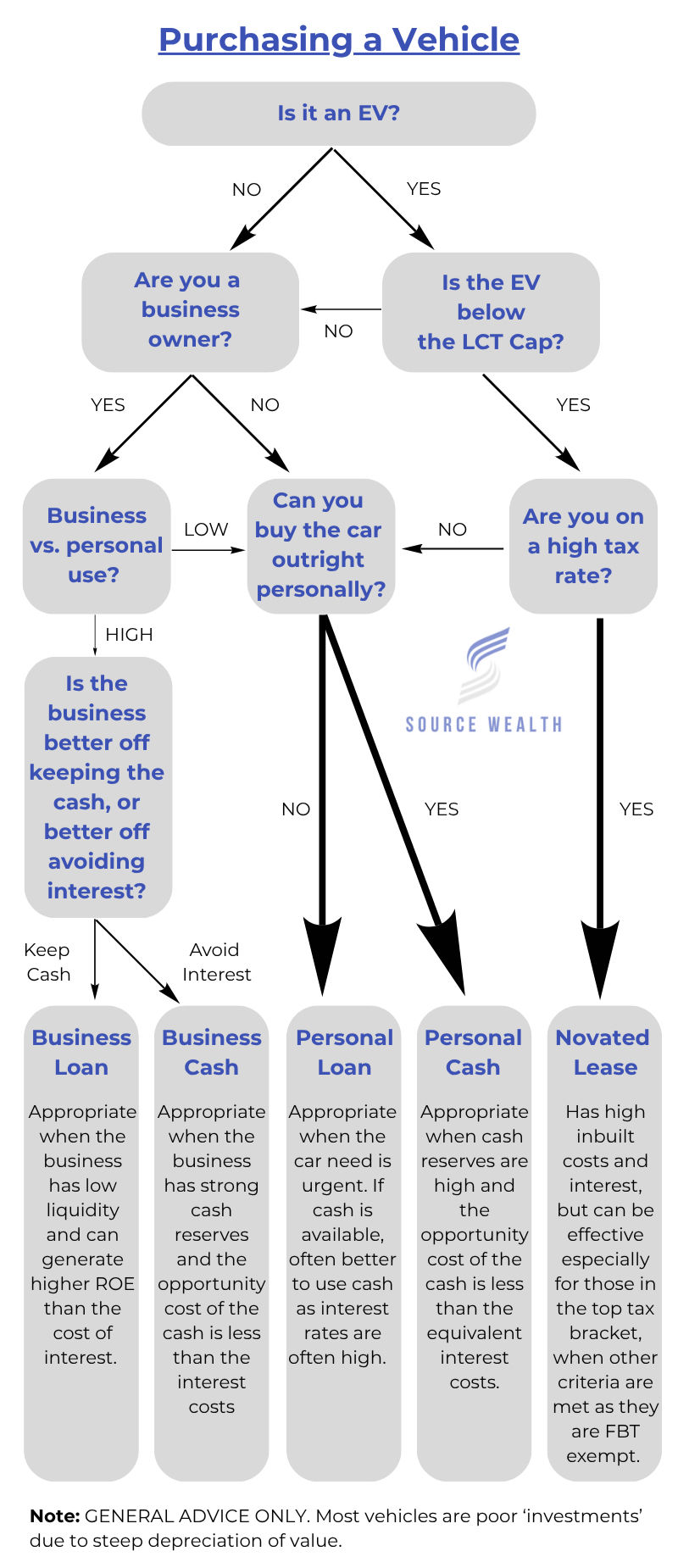

A decision tree like the one shown can be very helpful in stepping through the options and determining which may be the best decision.

The first questions in the decision tree is "Is the vehicle an EV?". This is important because fringe benefits tax (FBT) is not payable on the private use of EV vehicles that meet eligibility. This effectively allows you to salary‑package the entire cost of the EV tax‑free This incentive was introduced in 2022 to encourage the take up of electric vehicles. For clients on high marginal tax rates, and who want an EV, this tax benefit can be a compelling reason to establish a novated lease. Just be mindful that novated leases typically come with a balloon (lump sum) payment that is due after 5 years.

However, for clients who may not want an EV, or, if the car they want is above the Luxury Car Tax, novated leases are often a poor choice. Without the FBT exemption, the high inbuilt costs of novated leases often make them an inferior choice compared to the other available options.

For business owners who don't want an eligible FBT exempt EV, it is common to purchase the vehicle in the name of the business when the tax deductions outweigh the FBT. This is most common when business use is high and private use is low.

When the business owns the car, it can claim:

Depreciation (up to the car limit)

GST credits on the purchase and running costs

Running costs (fuel, servicing, insurance, rego)

Interest on a business car loan

For business owners, the choice of whether to use business cash or a business loan is all about opportunity cost. Ask yourself: "With this money could I generate a return on equity percentage that is higher than the cost of interest?"

For example, let's say you had $50,000 in cash that could be used to purchase a business vehicle that you need or you could use this cash to fund Google ads that bring in more customers. If the interest rate on a car loan is 7%, but the net ROE of the google ads is 15%, then from an opportunity cost perspective, you should fund the car via a loan and use the cash for marketing. Of course, if those percentages are switched, you should use cash instead to purchase the vehicle.

Opportunity cost is also an important consideration for non-business owners/employees. For instance, let's say you have ample funds available in your mortgage offset to purchase a car and still be left over with a sufficient cash buffer. The mortgage offset is offsetting a home loan interest rate of 5.5%. If you were to purchase a car, the car loan would be 7%. Therefore, from an opportunity cost perspective, it makes more sense to use cash to purchase the vehicle.

It's important to remember that most vehicle purchases are a poor investment decision. Most new cars depreciate 15% the second they are driven out of the dealership. Therefore, from a Financial Planning perspective, you should make sure you have the basics set up first before indulging in a nice new car. The basics are things like:

Having a cashflow buffer in savings of at least 3 months of living expenses.

Demonstrating a consistent savings capability each month.

Paying off bad debts first (things like credit cards, personal loans etc).

Purchasing your first home - remember car loans are another impediment in obtaining a home loan.

If you're a high‑income earner or business owner and want clarity on the smartest way to structure your next vehicle purchase, you can:

The purpose of this blog is to provide general information only and the contents of this blog do not purport to provide personal financial advice. We strongly recommend that investors consult a financial adviser prior to making any investment decision. The contents of the our blog does not take into account the investment objectives, financial situation or particular needs of any person and should not be used as the basis for making any financial or other decisions. The information is selective and may not be complete or accurate for your particular purposes and should not be construed as a recommendation to invest in any particular product, investment or security. The information provided on this blog is given in good faith and is believed to be accurate at the time of compilation.

Comments